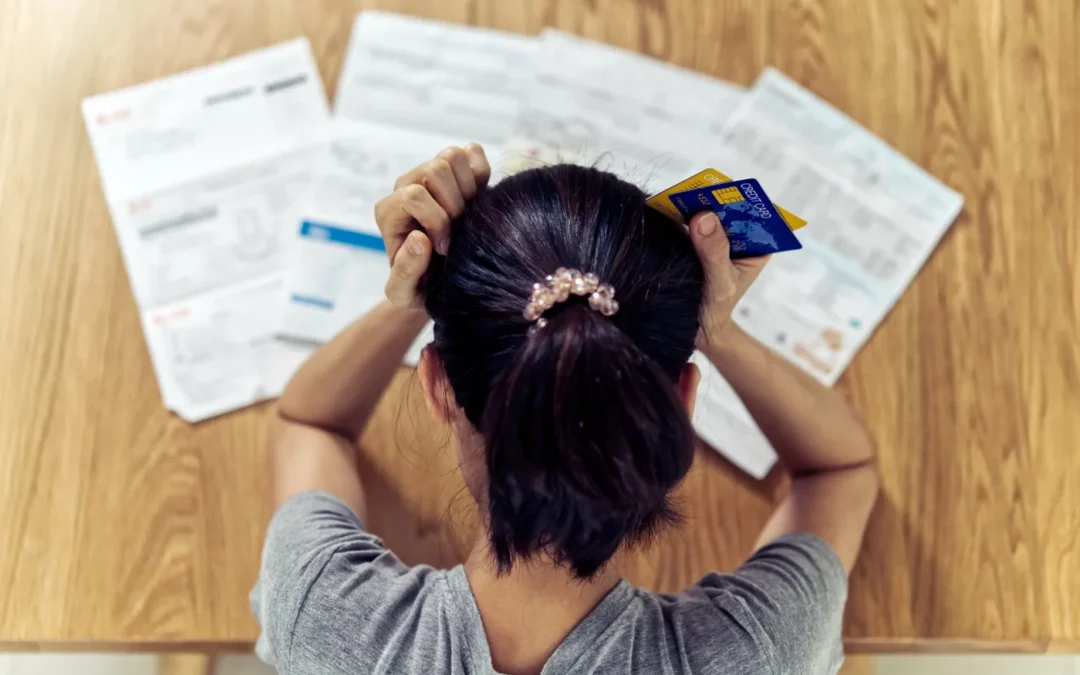

According to the Federal Reserve Bank of New York, credit card delinquencies during the pandemic have risen to nearly 10 percent. In Quarter 2 of 2020, the rate was 9.8 percent, inching toward the Great Recession record of 13.7 percent.

People miss credit card payments for a variety of reasons. In 2019, NerdWallet found that the most commonly cited reason was that the consumer simply forgot to make the payment. However, the next two reasons – lack of money and the money was needed for unexpected expenses — accounted for almost two-thirds of all incidents.

If you find yourself in a position of credit card delinquency — and even one month behind on a single card can negatively impact your credit score – contact the credit protection attorneys at Stecklein & Rapp. We have more than two decades of experience helping consumers like you in and around Kansas City, Missouri, Kansas City, Kansas, and Lincoln, Nebraska.

Common Reasons for Credit Card Delinquency

According to NerdWallet, the online service that tracks consumer credit and rates credit card companies, in mid-2020 total credit card balances across the U.S. reached $413.7 billion.

Debt, according to the site, also seems to skew by age and family obligations. For instance, young parents of children often carry more credit card debt than parents with grown or no children.

Relying on surveys from the Harris Poll, the company also found that the average revolving credit card debt in the U.S. came to $6,849 in 2019, with an average yearly interest charge of $1,162.

As for the reason consumers missed payments, as mentioned briefly above, NerdWallet found that 35 percent simply forgot; 33 percent needed the money to pay for essentials, and 32 percent needed the money for an unexpected expense. In other words, 65 percent of delinquencies were driven by money issues.

Consequences of Late or Skipped Payments

Often, in tough times credit card payments are subordinated to rent or mortgage payments and other necessities, including food, health care, transportation, and utilities, but if delinquency looms, you must be proactive.

Missed payments can result in costly consequences. The card issuer can charge up to a $29 penalty for your first missed payment, which can rise to $40 per missed payment within six billing cycles.

In addition, the credit card company can raise the interest rate on your account to as high as 29.99 percent. After 90 days, many issuers will cancel your card and send it to a collection agency.

The hit on your credit score can come rapidly as well. Once payment is 30 days late, the issuer can list your account as delinquent, which can result in an immediate loss of up to 110 points on your score. Your score will continue to drop as the months of missed payments add up.

If a compromise has occurred, call an identity theft attorney to help.

Avoiding Delinquency

If you know you can’t make a payment, you should contact the issuer and see if you can arrange a lower payment or negotiate an extended payment plan. It’s not in your best interests to avoid the debt obligations you have. You should reach out to your creditors, not disappear and hide.

Many credit card companies have established, often under government pressure, COVID-19 relief payment plans, which can stretch out your payment period, and even reduce or eliminate payments for a while. Of course, your total debt will stay on the books, and you’re expected to eventually honor it, but this pandemic relief effort can soften the blow and leave you with more cash for essentials.

To avoid missing a payment, you should consider some or all of these steps:

- Set up automatic bill pay

- Get your cellphone to send you text reminders or alarms when your payment is due

- If your bill is due at the most cash-strapped time of the month, contact the issuer to see if you can work out another due date

However, if things go south and making a payment is challenging, reach out to the issuer. Silence isn’t golden when it comes to credit.

Your Rights If Sent to Collections

If your debt is sent to a collection agency, you can expect endless phone calls, emails, and snail-mail reminders. What are your rights if this happens?

Debt collection efforts are governed by the Fair Debt Collection Practices Act (FDCPA), which is enforced by the Federal Trade Commission (FTC). Under the FDCPA, debt collectors are prohibited from:

- Calling you before 8 a.m. or after 9 p.m.

- Calling you at work once you inform them that your employer forbids such calls

- Involving friends, acquaintances, or other third parties associated with you in their collection efforts

- Harassing, abusing, or threatening you, or using obscene or profane language

- Lying about the amount owed

- Using deceptive tactics such as claiming to be law enforcement officials or attorneys when they’re not, or threatening to seize or sell your property

- If you want the emails and phone calls to stop, under the FDCPA you can send a letter to the collector asking them to stop. Once they receive the letter, their only options are to contact you to confirm the dunning notices will stop, or contact you to say they’re filing a lawsuit.

How Stecklein & Rapp Can Help

If you’re facing credit delinquency nightmares, the experienced attorneys at Stecklein & Rapp (formerly Consumer Legal Clinic, LLC) have been fighting for people in your situation for more than 20 years. Rather than trying to go it alone, you can rely on our team to discuss your situation with you and provide you with the best options available to resolve your dilemma.

With locations in Kansas City on both sides of the Kansas and Missouri state line, as well as in Lincoln, Nebraska, Stecklein & Rapp stands ready to assist you. Contact us today for a free initial consultation, and let’s get started securing your future.